Running a business takes courage, dedication, and hard work. However, it also requires basic knowledge about taxes so you can stay out of trouble, maximise your savings, and grow your business.

While taxation paves the way for improved public services, it also takes a big chunk out of a business’ profits. As a result, tax-abiding businesses have less money available for reinvestment, hiring, or paying out dividends to shareholders. The stakes are even higher for small businesses, especially those with tight margins as it is.

In Australia, for instance, small businesses have to comply with several tax regulations. These include income tax, goods and services tax (GST), payroll tax, and fringe benefits tax (FBT), among others.

Fortunately, there are also corresponding tax concessions and deductions that can help AU SMEs and entrepreneurs minimise taxes and maximise their savings.

Understanding Small Business Tax Relief in Australia

The Australian government values the role that small businesses play in its economy. With 3.2 million small businesses employing 5.6 million Australians, they are key to generating jobs.

As a way of giving back, the Australian Taxation Office (ATO) offers various tax relief measures to help these small businesses thrive. These tax reliefs can be in the form of tax concessions that enable small businesses to offset taxes.

This directly reduces the taxable income of eligible small businesses, offering a refundable offset of 16% of a small business’ net income and is capped at $1,000 per income year.

The Basics of Small Business Taxation in AU

Small businesses need to report their income accurately so that the ATO taxes them accordingly. The tax rates vary based on the structure. Fortunately, small businesses in AU are eligible for a lower tax rate of 27.5% compared to the 30% rate imposed on larger corporations. This reduced rate applies if their annual turnover is under $50 million.

Moreover, businesses with an annual turnover of $75,000 or more need to register for GST. This is the 10% tax on most goods, services, and other items sold or consumed in Australia. Registered businesses include this GST in their prices so they can claim corresponding credits during tax season.

Key tax rates and thresholds

The following is a rundown of the key tax rates and thresholds for small businesses in Australia:

- Income Tax – The standard rate for companies is 30%. However, a lower rate of 27.5% applies to companies with an annual turnover capped at $50 million.

- Goods and Services Tax – To comply with GST, a 10% rate is applied to most goods and services.

- Annual Turnover – Small businesses with an annual turnover of less than $10 million can also get additional tax concessions from the ATO.

Eligibility for Small Business Tax Relief

Eligibility for Small Business Tax Relief

Tax relief measures are meant to ease the financial burden of small business owners so they’ll keep operating. The Australian government periodically introduces measures to support the small business sector, in recognition of their role in sustaining countrywide employment.

Tax relief eligibility is based on specific turnover thresholds that are constantly updated, hence, the need to monitor the latest tax regulations.

Criteria for Small Business Tax Relief

A business’ aggregated turnover determines its eligiblity for small business tax relief measures. The aggregated turnover refers to the total income generated across all the businesses registered in your name.

Generally, your business’ annual turnover should be less than $2 million to qualify as a small business and for the corresponding tax concessions. This includes deductions for costs incurred in running the business such as staff wages, marketing, and other business finance costs.

Types of businesses that can benefit from tax relief strategies

A wide range of Australian businesses can benefit from different tax relief strategies, as long as they have an annual turnover capped at $2 million. These include:

- Sole Traders – These refer to individuals running their own businesses without a separate legal structure. They have full control over their businesses and are personally responsible for all aspects of operations.

- Partnerships – In partnerships, two or more people run a business together, sharing both profits and losses. Partnerships are governed by an agreement, outlining the terms and conditions including profit-sharing, decision-making authority, and each partner’s responsibilities.

- Small Proprietary Limited Companies – Also known as Pty Ltd, these are companies with certain ownership and turnover limitations. This means that a shareholder’s liability is limited to the extent of their shares in the company.

- Start-Ups – This refers to new businesses in their initial growth stages. They are often characterized by innovation, rapid growth potential, and scalability. Start-ups typically operate in emerging or high-growth industries, leveraging creativity, technology, and unique business models.

- Freelancers and Contractors – These are independent workers providing services to businesses or individuals. They usually work on contractual or project-based arrangements, and often fall under the self-employed category.

While these businesses vary in structure, most of them meet the $2 million turnover threshold, qualifying for most AU business tax relief benefits.

Tax Deductions for Small Businesses

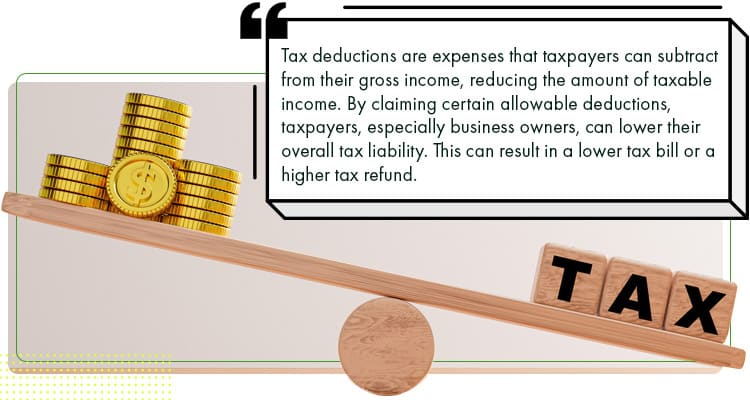

Tax deductions are expenses that taxpayers can subtract from their gross income, reducing the amount of taxable income. By claiming certain allowable deductions, taxpayers, especially business owners, can lower their overall tax liability. This can result in a lower tax bill or a higher tax refund.

Australian small businesses, for instance, can claim a variety of tax deductions to reduce their taxable income and minimise tax obligations. These include pre-paid business expenses, marketing and advertising costs, motor vehicle expenses, travel expenses, and bank fees, among others.

Immediate Write-Offs

Immediate write-offs is a form of tax relief that encourages businesses to invest in new equipment, technology, or other assets. It involves fully deducting the cost of a business expense or asset purchase from the taxable income in the year it was purchased. This way, it’s more strategic for businesses to get immediate write-offs instead of spreading the cost over several years through depreciation or amortisation.

There are different rules and limits for immediate write-offs. Some countries have specific thresholds for asset costs. Additionally, certain types of assets may not also qualify for an immediate write-off. This depends on the country and can change annually, depending on their respective tax laws and regulations.

Explanation of immediate write-offs and applicable limits

The Australian Taxation Office allows instant asset write-offs to eligible businesses. As a result, these organisations can claim an immediate tax deduction for the full cost of certain qualifying assets, reducing their taxable income for the year the assets are first used or installed.

Moreover, the Australian government increased the instant write-off threshold to $20,000. However, this is just a temporary measure and only applies to small businesses with an aggregated turnover of less than $10 million. Small businesses can avail of this for the 2023-24 income year – from 1 July 2023 until 30 June 2024.

Recent changes and how they impact small businesses

With the higher threshold, AU small businesses can claim the full cost of their eligible assets, significantly reducing their taxable income for 2023 and 2024. This translates to potential savings, allowing small businesses to reinvest in their business for growth or use the same to improve their cash flow.

However, the $20,000 threshold is temporary. After June 2024, it may revert to the lower $1,000 threshold. Hence, eligible businesses must plan their purchases accordingly to benefit from the increased threshold.

Depreciating Assets and Concessions

Depreciating assets refer to those with a limited useful life and will decline in value over time due to wear and tear. These include machinery, equipment, computers, furniture, and vehicles, among other company assets that reduce their value after long-term use.

By default, businesses cannot deduct the entire cost of a depreciating asset in the year it was purchased. Instead, they spread the cost out over the asset’s useful life. This is called depreciation: a non-cash expense that reduces a business’ taxable income.

On the other hand, concessions are special allowances, deductions, or tax breaks offered by the government to ease tax burdens. These incentivise certain types of business activities or support specific industries, encouraging economic and business growth. Done right, concessions can significantly reduce a business’ tax burden, improving its profitability and cash flow.

Sometimes, concessions can affect asset depreciation calculations. A good example is when governments offer increased depreciation rates for certain assets, such as the $20,000 instant write-off threshold allowed by the ATO.

Overview of depreciation rules for small businesses

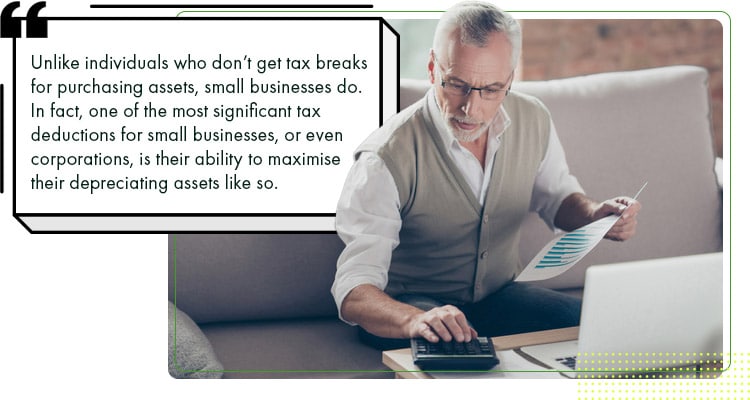

Small businesses can take advantage of their assets’ depreciation as a tax write-off. This is one advantage businesses have over ordinary taxpayers.

Unlike individuals who don’t get tax breaks for purchasing assets, small businesses do. In fact, one of the most significant tax deductions for small businesses, or even corporations, is their ability to maximise their depreciating assets like so.

Unlike individuals who don’t get tax breaks for purchasing assets, small businesses do. In fact, one of the most significant tax deductions for small businesses, or even corporations, is their ability to maximise their depreciating assets like so.

For instance, vehicles, machinery, and equipment are reasonably expected to decline in value over the time they are used. Thus, small businesses can use their depreciating value as a way to reduce their taxes.

How to claim deductions on depreciating assets

Here’s what you can do to claim these deductions:

- Determine the asset’s effective life;

- Choose a method for calculating the decline in value; and

- Calculate the decline in value for each income year.

If you need further assistance, the Australian Taxation Office provides comprehensive guidance for various asset types. You just need to determine the effective life of your assets and the appropriate methods for calculating the depreciation of each one.

Operating Expenses

Running a business can definitely be more difficult than working an 8-5 job. Unlike regular employment, it entails bigger risks. Therefore, the government provides incentives for business owners in the form of tax breaks and deductions which include Operating Expenses (OpEx).

Common operating expenses eligible for deductions

Operating Expenses refers ti the costs incurred by business owners in running their companies. Some of the most common examples include:

- Rent and utilities for business premises;

- Wages and salaries for employees;

- Insurance premiums (e.g. professional indemnity, public liability;

- Repairs and maintenance for business assets;

- Accounting and legal fees;

- Superannuation contributions for employees;

- Marketing and advertising expenses; and

- Other expenses related to business and its operations.

By allowing businesses to claim deductions for these operating expenses, the government incentivises corporations to reinvest their profits, enabling further business growth and expansion.

Tips for accurately tracking and claiming these expenses

Small businesses and big corporations alike must keep track of their OpEx to ensure that they claim all possible deductions.

This is why you need to keep detailed records of all business transactions such as receipts, bank statements, and other relevant documents. You can also make use of accounting software programs to help automate this process.

For some business owners, they track business expenses by:

- Opening a business account. Keeping track of business expenses is easier when you have a dedicated checking account for the business. This way, your operating expenses are all in one place, making it easier to claim tax deductions.

- Using an accounting software. The right accounting software can automate record-keeping and expense tracking,and ideally has reporting tools for year-to-year expense comparisons.

- Connecting to banks. You can further simplify things by linking your accounting software to your preferred banks. This enables the automatic download of all bank transactions and easier categorising of your business expenses.

- Filing receipts. Small businesses are required to keep relevant financial documents for at least three years. Thus, it helps to file your receipts, as well as indicating the purpose of each purchase.

- Reviewing business expenses. Lastly, review your expenses regularly, even if you have an accountant. Review the numbers to analyse your spending and identify specific areas where you can cut down.

Tax Credits and Incentives

As we mentioned earlier, small businesses can enjoy tax credits and incentives. In essence, a tax credit is the amount you can subtract directly from the taxes you owe.

This is different from tax deductions since these just lower the amount of your taxable income. Moreover, the amount you can deduct depends on your tax bracket.

In effect, tax credits are generally preferred because they directly reduce the taxes you owe.

Research and Development Tax Incentive

Australia values small businesses and corporations that contribute to both the economy and to research. Hence, the AU government provides tax credits to those who invest in creating innovative solutions and producing groundbreaking work.

The Research and Development Tax Incentive helps companies innovate and grow by offsetting a portion of eligible R&D costs.

Explanation of the R&D tax incentive

AU’s R&D Tax Incentive has allowed many growing companies to innovate.

By providing tax incentives, the government encourages small businesses, especially startups to work in agriculture, biotechnology, built environment, energy, manufacturing, mining, software development, and other sectors.

Eligibility criteria and application process

Small businesses can claim research and development tax offsets if they:

- Are an R&D entity; and

- Have incurred notional deductions of at least $20,000 on eligible R&D activities.

Furthermore, you’re considered an R&D entity if you’re:

- Incorporated under AU law;

- Incorporated under a foreign law but are an Australian resident for income tax purposes; or

- Incorporated under a foreign law and:

- A resident of a country with which AU has a double tax agreement; and

- Carrying on business in Australia through a permanent establishment.

Conversely, you’re not eligible if you’re:

- An individual;

- A corporate limited partnership;

- Any exempt entity; or

- A trust (except a public trading trust with a corporate trustee)

Small Business CGT Concessions

Aside from R&D, small businesses can also take advantage of Capital Gains Tax (CGT) concessions. These are tax credits from the sale of certain assets.

Normally, businesses have to pay taxes on the profits they gain from the sale of capital assets. Assets are typically items that play a key role in a business’ operations and profitability.

This, business owners can either reduce, disregard, or defer some or all of the capital gain from an active asset. This results in a lower taxable income, increasing the budget for reinvestment.

Capital Gains Tax (CGT) concessions available for small businesses

Australia has four small business CGT concessions, namely:

- Small business 15-year exemption – This applies when you continuously owned the CGT asset for 15 years before its sale;

- Small business 50% active asset reduction – This concession applies automatically when you own the asset for more than 12 months – unless you opt for the other CGT concessions;

- Small business retirement exemption – This applies when you’re ineligible for the small business 15-year exemption; and

- Small business roll-over – This is applicable when you acquire an asset replacement or incur costs to make capital improvements to an existing one.

Tax Planning Strategies for Small Businesses

Dealing with taxes may be challenging, but proper planning can make this more manageable.

For instance, big corporations hire a team of accountants, compliance officers, and tax experts to deal with their taxes. Meanwhile, small businesses make use of eligible deductions and strategic structuring to optimise tax efficiency.

In both instances, these key strategies are crucial:

- Keeping accurate records – Have an accurate and detailed record of all business-related income and expenses.

- Claiming eligible deductions – Small or big businesses alike should claim all allowable deductions including capital allowances, business expenses, and depreciation.

- Creating a tax-effective business structure – Be strategic in designing your business model. Choose a structure that is tax-efficient but still aligns with your business goals.

Structuring Your Business for Tax Efficiency

Running a business is all about strategy. You have to use the right ones for product differentiation, innovation, and operations – including your business structure.

Done right, you can minimise your tax liabilities, resulting in bigger profits. Moreover, leveraging tax deductions, credits, and incentives relevant to your industry can further optimise your tax position.

Therefore, it’s crucial to structure your business for tax efficiency, allowing you to retain more of your hard-earned money and ensure financial success.

Considerations for choosing the right business structure (sole trader, partnership, company, or trust) for tax purposes

Businesses come in many forms and operate differently. Some are run by a single person, while others are managed by groups or even other corporations. Consequently, they have different tax liabilities.

Let’s take a look:

- Sole Trader – It’s simple and easy to set up since it’s owned and operated by an individual. However, this set-up offers limited tax benefits such as OpEx, vehicle expenses, work-from-home expenses, and instant asset write-offs.

- Partnership – Partnerships are not subject to income tax but they’re required to lodge a partnership tax return each income year. Since a partnership doesn’t have a separate legal personality, each partner carries the net income or loss.

- Company – Corporations enjoy various tax benefits such as concessions, offsets, and rebates. However, they also have to comply with various requirements in the process.

- Trust – This offers numerous tax benefits and asset protection options, including a 50% CGT discount for family trusts. But this can be complex to set up and manage.

Superannuation Contributions

Many small businesses also consider superannuation contributions as part of their tax planning strategies.

Superannuation contributions are payments made to a long-term savings plan to help individuals save for retirement. This is compulsory and requires AU employers to make regular contributions on behalf of their employees.

The role of superannuation in tax planning

Small businesses contributing to their employees’ superannuation funds are eligible for tax benefits.

For example, if your small business has a gross income of $250,000, and you contributed $25,000 to your employees’ superannuation funds, you can deduct the latter from the former. This reduces your taxable income to $225,000.

Contribution limits and tax benefits

The ATO has set annual contribution limits and exceeding them could result in penalties. Here are some of the concessional contributions caps in recent years:

- $30,000 – Beginning 1 July 2024

- $27,500 – From 1 July 2021 to 30 June 2024

- $25,000 – From 1 July 2017 to 30 June 2021

If you were unable to maximise your contribution caps from previous years, you may be able to carry these forward to increase your contribution caps in later years.

Loss Carry-Back Tax Offset

Businesses, when managed well, can generate profits, but they are not immune to losses.

Guess what? This can be in your favour.

The AU government allows certain business establishments to apply tax losses incurred in a particular year against their taxable income from previous years.

How small businesses can offset current year profits with previous losses

According to the ATO, eligible small businesses can get the offset by choosing to carry back losses to earlier years in which they had income tax liabilities.

For example, your business had a taxable income of $200,000 in 2021-2022 and you paid $55,000 in taxes. In 2022-2023, you had a taxable income of $300,000. However, your company incurred a loss of $250,000 in 2023-2024.

Fortunately, you can choose to carry back this loss to offset your taxable income in 2021-2022 and 2022-2023. In other words, you can potentially get a refund of the taxes paid up to the amount of the loss, subject to certain limitations.

Application process and limits

Small businesses that want to claim the tax offset for an income year need to choose the loss carry back choice when they lodge their company tax return for that year.

You will need to provide:

- Your opening and closing franking account balance;

- Your aggregated turnover for each loss year;

- The amounts of the tax losses you’re carrying back;

- Your tax liability for the income years you’re carrying the loss back to; and

- The amounts of unutilised net exempt income for the income years you are carrying the losses back to.

At the moment, the offset cap is at $5 million, and the business must have had a tax loss in the previous year.

Common Mistakes Small Businesses Make in Claiming Tax Relief

Tax errors can be stressful and costly. They can also be frustrating, especially when you miss out on eligible deductions due to avoidable mistakes or neglect. Worse, you may even have potential issues with tax authorities.

Here are some of the most common ones to look out for:

Misclassification of Expenses

Businesses are highly encouraged to track down all operating expenses that can be deducted from their taxable income.

However, small businesses are prone to incorrectly categorising their expenses. They either place them in the wrong accounts or mix up personal and business expenses. Such errors greatly affect financial reporting and tax liability.

To avoid this, small businesses should implement strong accounting practices. In fact, some AU business owners outsource accounting and tax compliance to professionals. This way, expenses are correctly classified and compliant with tax regulations.

Inaccurate Reporting

There’s also a high risk of submitting incorrect or incomplete financial information. This happens when businesses lack an understanding of accounting principles and tax regulations.

Simple mistakes such as an overlooked invoice or incorrectly recorded sale can distort revenue figures, affecting profitability assessments and tax calculations.

Sometimes, business owners recognise revenue before it’s actually earned or defer expenses incorrectly. Both of these can inflate or deflate profits, leading to inaccurate reporting or even legal repercussions.

Neglecting to Claim Eligible Deductions

Eligible deductions help businesses maximise profits.

However, many business owners fail to claim deductions due to the lack of awareness, inadequate record-keeping, or a misunderstanding of tax laws and regulations. The most commonly neglected deductions usually include:

- Vehicle expenses;

- Home office deductions;

- Professional development and training expenses; and

- Bad debts.

By thoroughly understanding and claiming all eligible deductions, small businesses can reduce their tax burden and use the savings to grow their companies further.

FAQs

Here are some of the most frequently asked questions businesses get about tax relief:

How often do tax relief policies change in Australia?

Just like in other countries, tax relief policies in Australia are subject to change.

This often occurs during annual budget updates. Therefore, it’s essential for small businesses to stay informed and adapt to any changes, particularly in their respective industries.

Can new businesses also benefit from these tax relief measures?

Absolutely! The Australian Taxation Office allows new businesses to benefit as long as they qualify for the available tax relief measures.

As such, it’s crucial to understand the specific requirements and limitations for each measure. These are all found in ATO’s official website.

Conclusion

Small businesses are the driving force behind Australia’s economy. The Monarch Institute calls them “The Australian Necessity.” This is backed by a number of tax incentives and offsets available to help these businesses survive and thrive amidst the constantly evolving economy.

It’s therefore important for small businesses to understand and utltise these tax relief strategies.

To recap, you can structure your business for tax efficiency, make superannuation contributions, and avoid the common mistakes AU business owners fall for. By doing these and more, you can maximise your savings and expand your business faster.

- Want AI prompts to help you make faster and better business decisions? Check out these 100 AI prompts.

- How about a list of the Top Business Apps that could take your company to the next level this 2024? Head over here.

- Ready to hire world-class, high-performing virtual staff at 40% to 60% cost savings and lifetime support? Click here.

- Check out our 1,000 fully vetted and highly talented staff here.

Syrine is studying law while working as a content writer. When she’s not writing or studying, she engages in tutoring, events planning, and social media browsing. In 2021, she published her book, Stellar Thoughts.